Creating models that evaluate the real market value of crypto-assets is one of the pivotal challenges of the space. While the valuation methodologies for crypto-assets are still in its infancy, we can draw inspiration from many ideas from the quantitative investing world. As a completely digital asset, quant models are likely to be dominant in the crypto space but there is still a wide gap between both schools of thought. Adapting quant ideas to crypto-assets is not only intellectually fascinating but, arguably, one of the most effective mechanisms to develop valuation models for this new asset class. Today, I would like to explore one of my favorite new quant theories in the context of crypto assets: the quality minus junk(QMJ) factor.

The QMJ thesis is part of a broader branch of quant strategies known as factor investing. Conceptually, factor investing focuses on identifying key elements that are quantitatively influential in the behavior of a security and that can be combined to formulate different trading strategies. The history of factor investing can be traced back to a few seminal papers. In 1976, Stephen A. Ross published a paper on arbitrage theory in which he explained that returns on different securities could be explained using a handful of factors. In 1985, economists Barr Rosenberg, Kenneth Reid, and Ronald Lanstein published a paper titled “Persuasive evidence of market inefficiency” in which they presented a series of strategies that exploit market inefficiencies in equities. The most important academic milestone in factor investing was the publication of “The Cross-Section of Expected Stock Returns” by economics legend Eugene Fama and Kenneth R. French in 1992. That paper open the floodgates to numerous theories about factor investing including the controversial efficient market hypothesis.

Even though there have been variations of this idea, factor investing theory recognizes two main types of factor: macro and style. The former captures broad risks across asset classes while the latter aims to explain returns and risks within asset classes.

Over the years, factor investing has evolved from 3–4 key factors in the original Fama-French theory to over 400 in modern quantitative theory. The emergence of technologies such as machine learning has facilitated the discovery of new factors to the point that is hard to distinguish good ideas from others that are purely speculative without any math rigor. The discovery of new factors is often accelerated by the emergence of new asset classes. From that perspective, crypto-assets are likely to generate groups of new factors that are very tailored to the characteristics of this new asset class. Many of those factors will be adaptations of existing quant theories like our famous QMJ thesis.

Inside the QMJ Thesis

The QMJ thesis was originally by quant legend and AQR CEO Clifford Asness and his AWR colleagues Andrea Frazzini, and Lasse Heje Pedersen. The original paper was published in 2013 and has been revisited multiple times over the years. The main idea behind the QMJ thesis is remarkably simple as it studies the tendency for “high quality” stocks to generate alpha relative to “low quality” stocks. Obviously, the definition of “quality” is the core contribution of the QMJ thesis. In the QMJ paper, quality is defined based on three underlying factors:

Quality=f(Profitability, Growth, Safety)

- Profitability: They measured profits (per unit of book value) in several ways, including gross profits, margins, earnings, accruals and cash flows.

- Growth: This was calculated over the period spanning from the prior five years in each of their profitability measures.

- Safety: They assessed both return-based measures of safety (e.g., market beta and volatility) and fundamental-based measures of safety (e.g., stocks with low leverage, low volatility of profitability, and low credit risk).

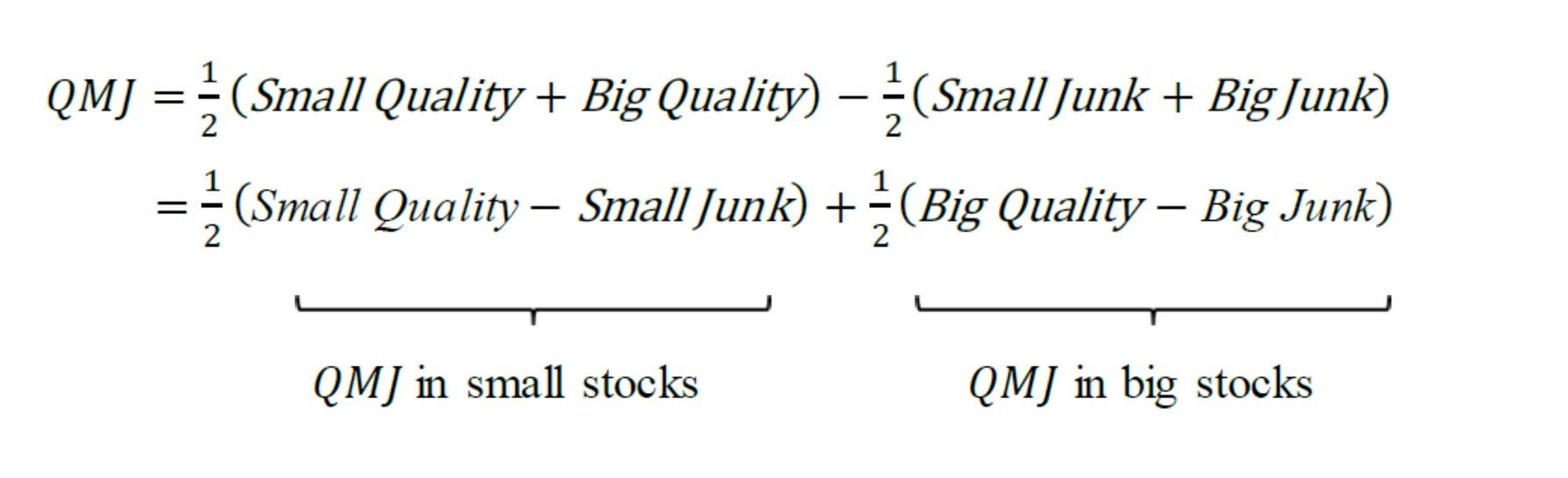

Based on that definition of quality, the QMJ outlines that you can construct a portfolio with long positions on the top high-quality stocks and short positions on the low-quality stocks relative to other factors such as value, momentum and size. The portfolio constructions can be summarized in the following pseudo-formula:

Without getting into all the details, QMJ portfolios have shown to outperform other equity portfolios, including high-quality exclusive portfolios, over the last few decades.

The QMJ Thesis and Crypto Assets

Back to crypto land, we can think about a few metrics that will represent the key underlying factors of quality: profitability, growth and safety. Let’s explore a few ideas:

Profitability Factors

In the Money Momentum

IntoTheBlock’s In-Out Money signal provides a statistical distribution about the positions of investors relative to the current price. The analysis describes percentages of investors that are realizing gains or losses based on their historical positions and the current price of the crypto asset. Similarly, IntoTheBlock’s In-Out Momentum factors the evolution of in-the-money positions over certain periods of time.

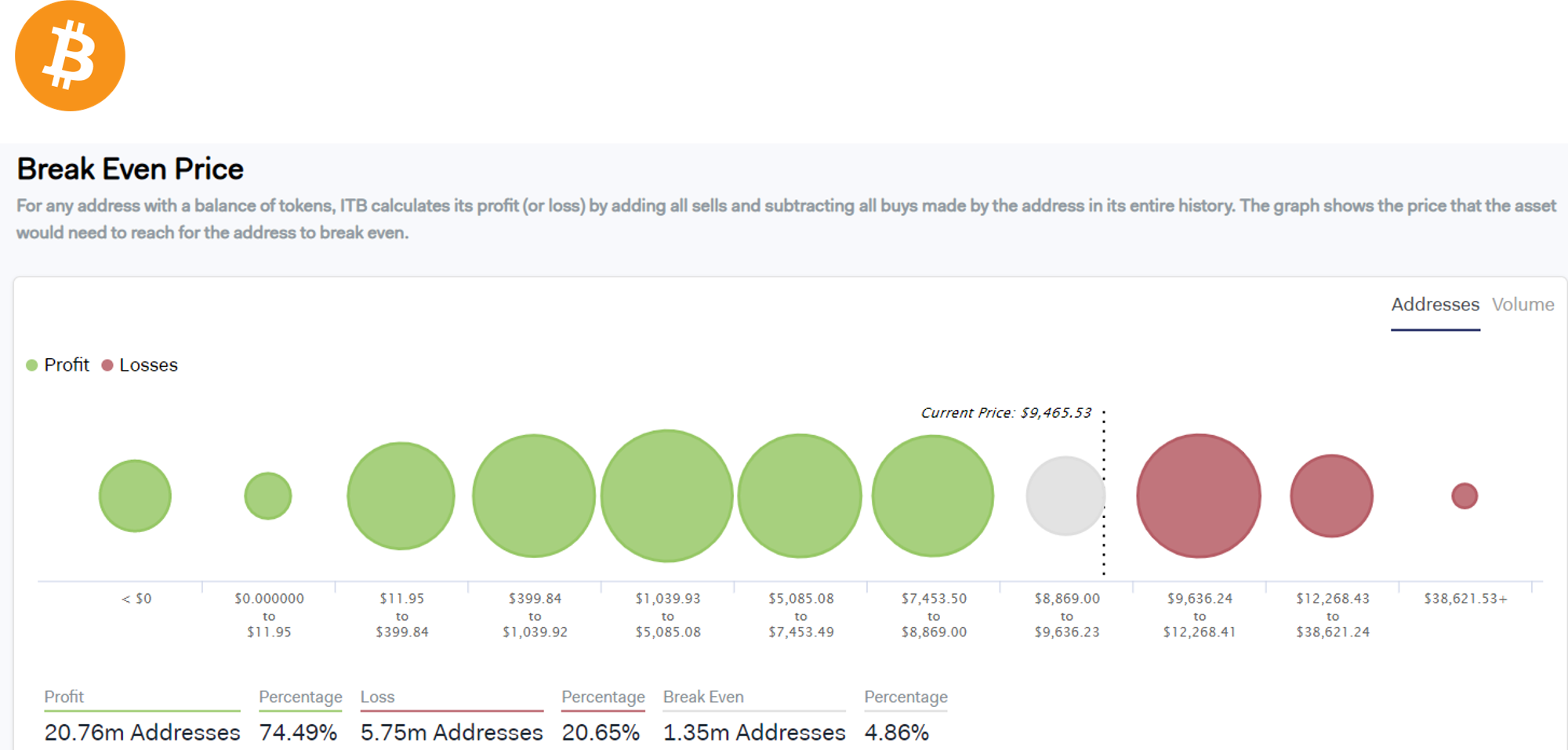

Break Even Price

IntoTheBlock’s Break-Even Price signal provides an analysis about where the price of a crypto asset should trend for different groups of investors to recuperate their investment. This is another indicator of the profitability distribution in a crypto asset.

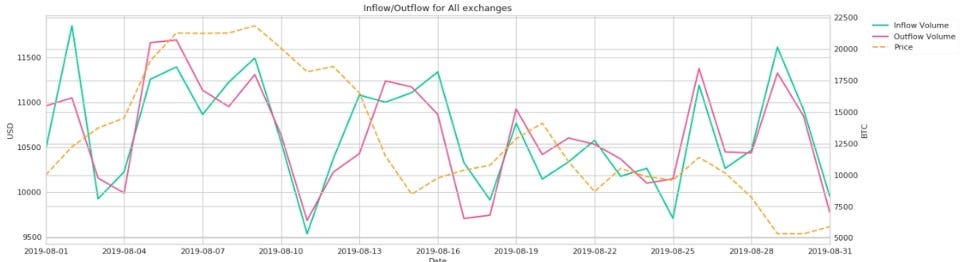

Exchange Fund Flows

Exchange money flows are another relevant indicator of the profitability of a crypto-asset. Relevant net flows into centralized exchanges are a positive indicator of the health of a crypto-asset. IntoTheBlock’s upcoming exchange netflow analysis provides an objective view into this dynamic.

Growth Factors

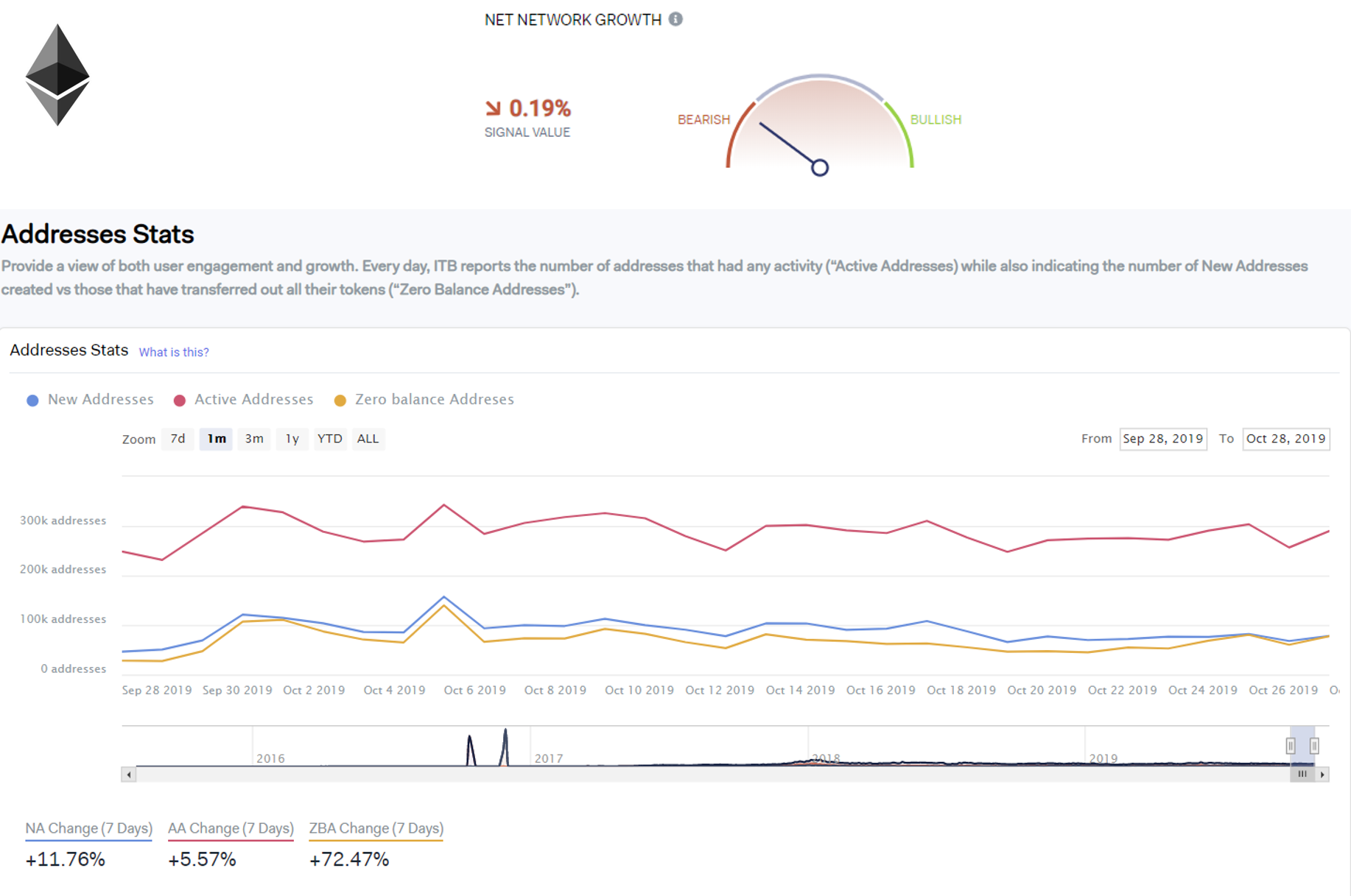

Net Network Growth

As network-based assets, the behavior of the underlying network is a relevant indicator of the growth of the crypto-asset. IntoTheBlock’s Net Network Growth measures the difference between new addresses being created and those whose balance goes to zero. Similarly, the Net Network Growth Momentum measures that signal over certain periods of time to provide bullish or bearish momentum on a specific crypto-asset.

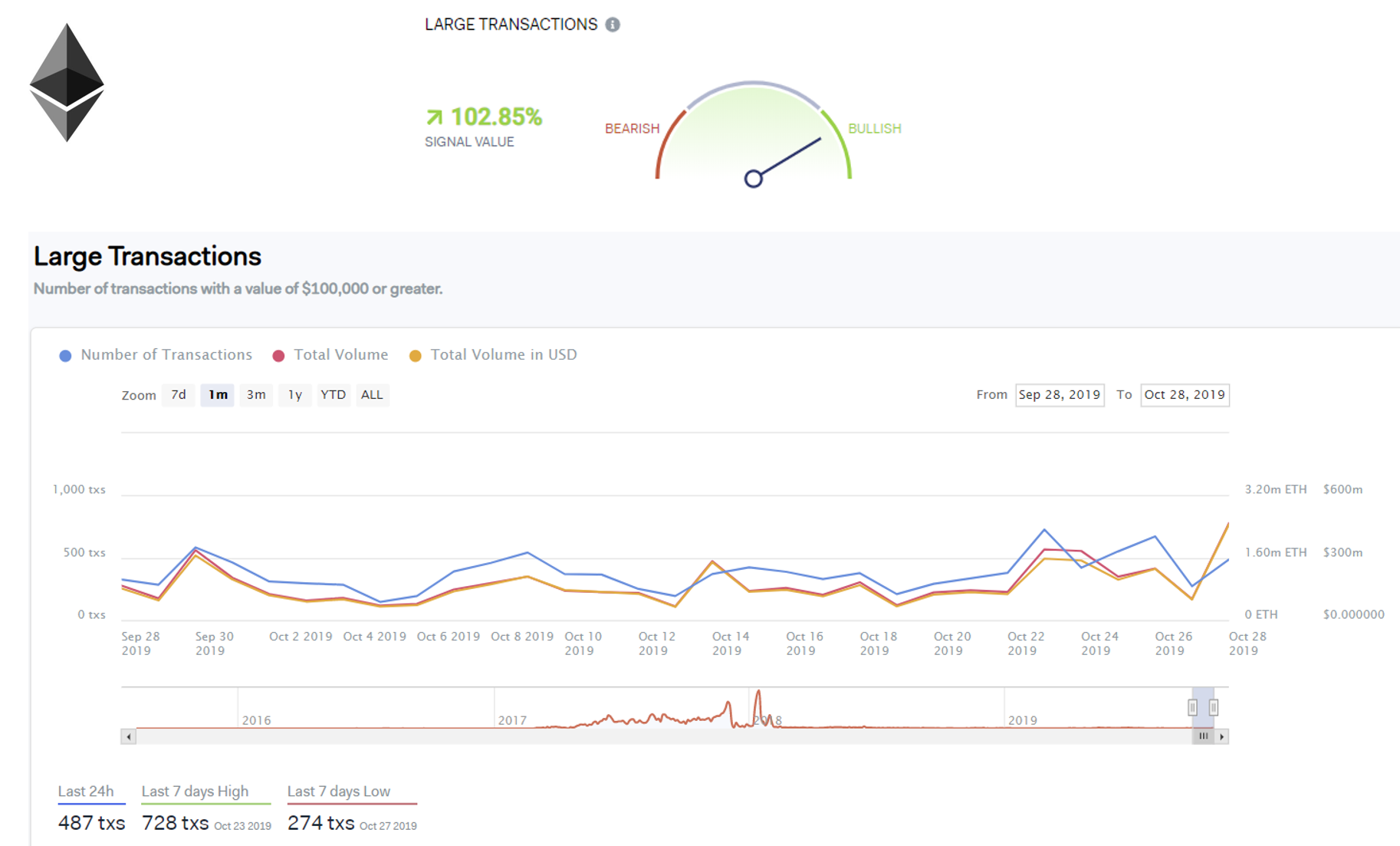

Large Transaction Momentum

Large transactions are another important sign of growth in a crypto-asset. IntoTheBlock’s Large Transaction analysis computes the trend of disproportionally large transactions over time. This signal is accompanied by a momentum indicator that provides a bullish or bearish sign based on the trend.

Safety Factors

Volatility

Volatility is a classic measure of safety in crypto-assets. IntoTheBlock’s Liquidity Analysis reflects this behavior.

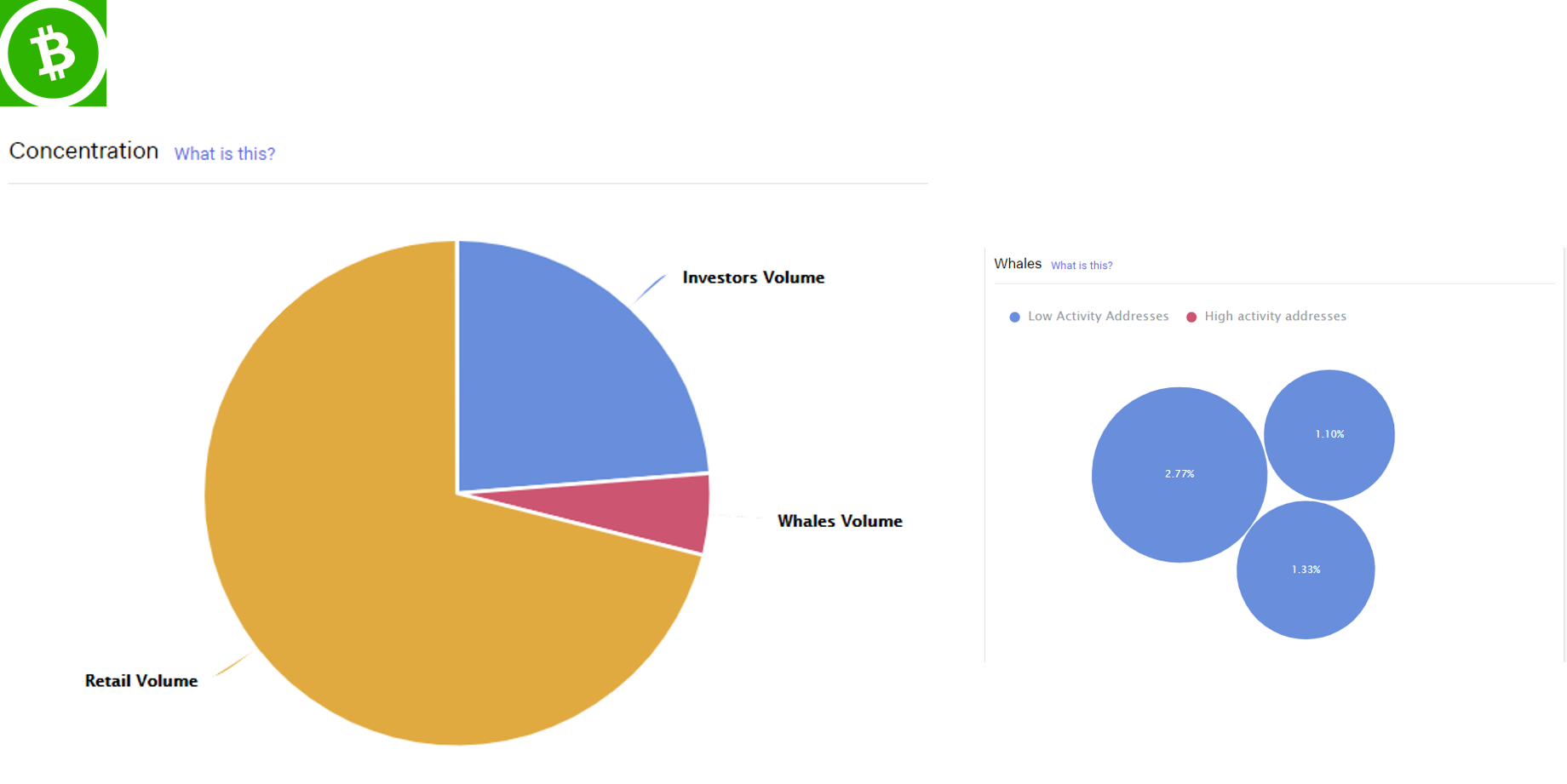

Whales Behavior

Whales play a relevant factor in crypto-assets. IntoTheBlock’s Whales analysis measures the behavior of whales in a given crypto-asset. Similarly, the Whales Momentum indicator measures the behavior of whales over time.

The combination of these and similar factors could help to adapt the QMJ thesis to crypto assets. Profitability, safety and growth factors can help us define new measures of quality (and junk) for crypto assets that enable better portfolio creation in the space.